The balanced scorecard (BSC), in its various forms, is one of the most popular and influential management ideas ever developed. According to a 2010 annual survey by Bain & Company, it was found to be the most widely used performance management framework in the world.The BSC was popularised by Robert Kaplan and David Norton. In 1992, the pair wrote an article for Harvard Business Review called “The Balanced Scorecard: Measures That Drive Performance,” which had a major impact on management thinking at the time. Several companies adopted the framework initially laid out in the HBR article and it eventually gained prominence throughout the world thanks to a subsequent book, “The Balanced Scorecard: Translating Strategy into Action” (1996), as well as many other additional books and articles published by different authors over the years.

Kaplan and Norton are sometimes referred to as the originators of the BSC, but this is not technically correct. The term "balanced scorecard," as well as the basic idea and framework, was first created and implemented by Art Schneiderman in 1987, then the VP of Quality and Productivity Improvement at Analog Devices Inc (ADI), a mid-sized semiconductor company. Kaplan and Norton encountered Analog Devices while at a research arm of KPMG in 1990 and became interested in Schneiderman's work as part of a case study analysing what 12 of the most successful companies were measuring at the time. The research from the study was used as the basis of their HBR article, in which they refer to a fictitious company called Electronic Circuits Inc (ECI) to illustrate the idea of the balanced scorecard. (ECI was in fact a pseudonym for Analog Devices.)

Both Kaplan and Norton acknowledge the important insights from many authors, consultants and thinkers in the field of performance management and strategic thinking that helped them to develop their own ideas, which have evolved considerably since the "first generation" BSC was introduced. Some of the most notable included the work done by French process engineers in the early 1900s who created the “Tableau de Bord” (dashboard of measures), the pioneering work of General Electric on performance measurement reporting in the 1950s, and Peter Drucker’s concept of "management by objectives," also introduced in the same decade, who popularised the saying, “If you can't measure it, you can't manage it.” This last idea is at the very foundation of the balanced scorecard.

Overview:

There is no standard or official way of describing the balanced scorecard (BSC), which has multiple descriptions and definitions. One of the most common is provided by Kaplan and Norton:

"The Balanced Scorecard (BSC) translates an organisation’s mission and strategy into a comprehensive set of performance measures that provides the framework for a strategic measurement and management system. The scorecard measures organisational performance across four linked perspectives; financial, customer, internal business process, and learning and growth."

Because the concept is presented and interpreted in many different ways, it has led to some confusion over whether it is best understood as a tool, system, approach or philosophy. Many authors have noted that the BSC was at one time a simple performance management tool, but has since evolved into a more holistic management system (with multiple pieces), although this might be considered an academic distinction as many people still refer to it as a management tool. This issue was astutely identified by EAB Group:

"The term Balanced Scorecard has multiple meanings. The initial meaning, when it was first popularised in early 90s, was of an approach for generating a performance report, by grouping performance measures by perspectives, the most commonly used being: Financial, Customer, Internal Processed and Innovation and Learning. Gradually, this management tool evolved to become the foundation of a performance management system that uses strategic, operational and individual performance plans as the basis for a communicating, monitoring and improving organisational performance. Its main components are the Destination Statement, the Strategy Map and the list of KPIs structured in 4 perspectives: Financial, Customer, Internal Processes, People, Innovation and Learning."

The “balanced” part of the scorecard refers to the fact that it takes into account more than just financial aspects of corporate performance. For example, if management decided to cut the number of staff working in a customer service department, then it may provide the company with a short-term gain through cost savings, but the balanced scorecard approach would take into account the impact on future earnings due to poor customer satisfaction.

The BSC was originally proposed by Kaplan and Norton as an alternate to traditional ways of measuring corporate performance. The key problem they had observed of companies at the time was that they tended to manage their businesses based solely on financial measures ("lag indicators") of past performance, which ultimately encouraged short-term thinking over long-term value creation. Kaplan and Norton have equated this approach to driving a car based on what you see in the rearview mirror. By focusing on 3 other core perspectives in addition to the financial perspective (making 4 core perspectives in total), an organisation can focus on "lead indicators" to ensure its future profitability.

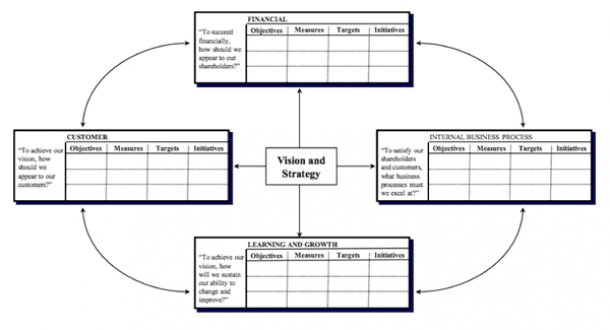

“[The image below] shows the original structure for the balanced scorecard (BSC). The BSC retains financial metrics as the ultimate outcome measures for company success, but supplements these with metrics from three additional perspectives — customer, internal process, and learning and growth – that we proposed as the drivers for creating long-term shareholder value.” — Kaplan

Fig. 1, The Balanced Scorecard, Kaplan and Norton, 1992

Fig. 1, The Balanced Scorecard, Kaplan and Norton, 1992

- Financial: (e.g., revenue, profit, rate of return, cash flow)“To succeed financially, how should we appear to our shareholders.”

- Customer: (e.g., market share, customer satisfaction, customer retention)“To achieve our vision, how should we appear to our customers.”

- Internal Business Process: (e.g., productivity rates, quality measures, delivery time)“To satisfy our shareholders and customers, what business processes must we excel at?”

- Learning and Growth: (e.g., engagement, satisfaction, turnover, skills and capabilities)“To achieve our vision, how will we sustain our ability to change and improve?”

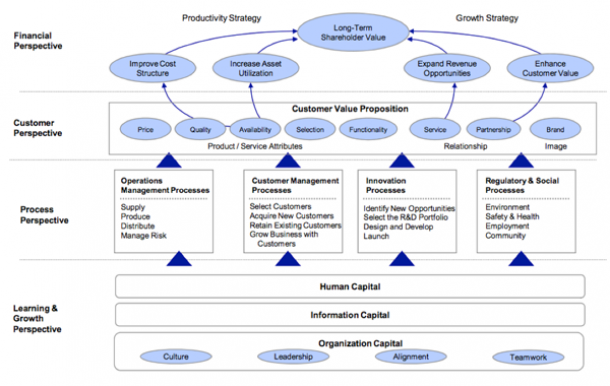

One of the most important additions to the balanced scorecard theory is the “Strategy Map” proposed by Kaplan and Norton in 2001. The Strategy Map (see Fig. 2) is sometimes so synonymous with the term "balanced scorecard" that, for some people, they are one and the same idea.

Fig. 2, The Strategy Map, Kaplan and Norton, 2001

The map shows a logical, step-by-step connection in the form of a cause-and-effect chain. It helps tell the story of how each area affects the success of the next. Learning & Growth (the bottom row) enables the organisation to improve its Internal Processes (the next row), which in turn enables the organisation to create desirable results in the Customer zone and thus achieve its Financial goals.

While many different descriptions exist for explaining the BSC, the general focus of the approach is about seeing organisational performance as a whole system that reflects a balance between providing short- and long-term objectives, financial and non-financial measures, “lag” and “lead” indicators, and between external and internal performance perspectives.

Sources:

- The Balanced Scorecard: Measures That Drive Performance, HBR, Kaplan and Norton, 1992

- The Balanced Scorecard: Translating Strategy into Action (1996), Kaplan and Norton

- The Strategy-Focused Organisation: How Balanced Scorecard Companies Thrive in the New Business Environment (2001), Kaplan and Norton

- Conceptual Foundations of the Balanced Scorecard, Harvard University, Robert S. Kaplan, 2010

- Analog Devices: 1986-1992, The First Balanced Scorecard, Arthur M. Schneiderman, 2006

- The Balanced Scorecard: Historical Development and Context, Karl R. Knapp, 2001

- Balanced Scorecard Typology and Organisational Impact, Aurel Brudan, actKM Online Journal of Knowledge Management, Volume 2, Issue 1, 2005

- Business Balanced Scorecard, From Concept to Implementation, KPMG India, 2011

- Brief History of the Balanced Scorecard, Kaizen Consulting Group, 2014

- 50 Ideas You Really Need to Know: Management (2012), Edward Russell-Wallin

- A Handbook of Management Techniques (2001), 3rd Edition, Michael Armstrong

- Business Process Management and the Balanced Scorecard (2007), Ralph F. Smith

- Balanced Scorecard, Bain & Company, May 2013 (Bain.com)

- The Balanced Scorecard Institute (Balancedscorecard.org)

- Balanced Scorecard Australia (Balancedscorecardaustralia.com)

- Balanced Scorecard (eabgroup.com.au)

- About the Balanced Scorecard (Balancedscorecardreview.com)

This article offers an expanded description of the summary listed in our post 40 Must-Know HR, OD, L&D Models.

We Would Like to Hear From You (0 Comments)